RISR & FIXP Commentary for May 2026

Click here for a pdf version of this commentary.

RISR Performance Summary

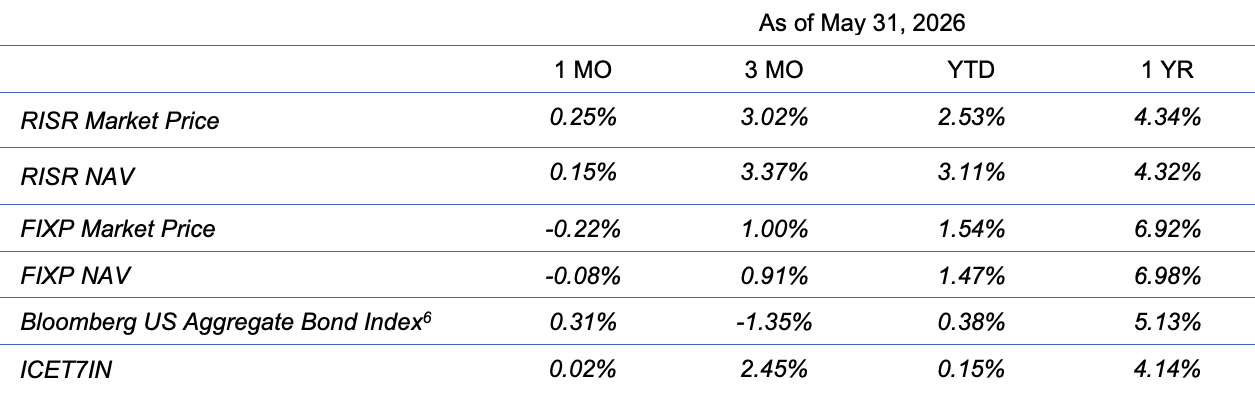

The FolioBeyond Alternative Income and Interest Rate Hedge ETF (ticker: RISR) returned 0.25% based on the closing market price (0.15% based on net asset value or “NAV”) in May. In comparison, the ICET7IN Index (US Treasury 7-Year Bond Inverse Index) returned 0.02% while the Bloomberg Barclays U.S. Aggregate Bond Index ("AGG") returned 0.31% during the same period.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling 866-497-4963. Short-term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. Returns beyond 1 year are annualized.

A fund's NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the fund was traded. The fund intends to pay out income, if any, monthly. There is no guarantee that these distributions will be made.

Total Expense Ratio is 1.04%.

For standardized performance click here.

May was another month of roller-coaster hope and despair over the situation in Iran and the greater middle east. The first half of the month saw a sharp increase in interest rates as rising oil prices from the closing of the Strait of Hormuz led to expectations of future inflation. This was reflected by the highest reported CPI and PPI[1] levels in three years, of 3.8% and an eye-popping 6.0%, respectively. Accordingly, RISR’s share price moved from 36.20 to 36.64 by May 19, an increase of 1.2%. Market sentiment reversed sharply after that as President Trump began to express confidence that a deal to end the conflict with Iran was at hand. Despite the fact that more than a dozen such claims had been made since the start of the war, with no peace materializing, interest rates and oil prices fell back down to end the month below the levels seen at the start of May.

In short, May was yet another month of alternating waves of despair/worry and hope/confidence that have dominated markets since the start of the war in February. It seems this pattern will continue until a sustained end to the conflict is reached, although when that may occur is anyone’s guess. The good news for RISR investors is that overall, the share price volatility is ameliorated to a large extent by the current income received from our MBS IO holdings. This is by design, of course, and is a big part of the reason RISR’s total return as compared to volatility remains greater than that of the broader bond market.

Return Sharpe Ratio[2]

RISR 0.352

AGG 0.289

There were more signs of stability in the labor market in May. Both new jobs and the unemployment rate were reported better than consensus expectations. This further lowered, some would say eliminated, any likelihood of additional cuts in the Fed Funds rate for the balance of the year. The new Fed Chair Kevin Warsh was sworn in during the month, but he provided no indication at his swearing in ceremony as to his thinking on any policy shift. Warsh’s views do not fit neatly into the dove/hawk paradigm markets like to employ. He has expressed concern about the size of the Fed’s balance sheet, but also has suggested that he might be less inclined to raise rates than some other board members.

The other Fed announcement was that outgoing Chair Powell announced formally he would be keeping his board seat until the final resolution of the pending investigations and threatened litigation into him and other Fed board members. This was largely expected, but the Trump Administration has provided very little evidence that they intend to drop matters. So, we could be looking at a current and ex Fed Chair attending meetings and voting on policy for some time: Powell’s board term doesn’t end until January 2028. The last time this occurred was when former chair Marriner Eccles continued to serve on the Fed Board of Governors from 1948 to 1951.

RISR has continued to attract investor funds. Since the beginning of the year AUM has increased by more than 35%, and we received capital inflows of around $23 million in May, which brought total fund assets to more than $250 million. This is an important threshold, because several large and important ETF distribution platforms require AUM of $250 million for eligibility. Now that RISR has reached that level, we are hoping to gain access to an even larger audience of RIAs and other asset managers through these platforms, which could help spur further growth in assets and improve liquidity for existing investors.

[1] Consumer Price Index; Producer Price Index

[2] Source: Bloomberg. Return Sharpe Ratio is measured as excess performance with respect to the 3- month risk free rate per unit of volatility over the time frame. Performance is measured as mean return.

FIXP Performance Summary

FolioBeyond’s Enhanced Fixed Income Premium ETF (ticker: “FIXP”) seeks to provide income and, secondarily, long-term capital appreciation. The Fund invests in a portfolio of ETFs representing certain sectors of the fixed income market. In addition, the Fund seeks to generate additional income by writing options on these same ETFs, or other ETFs we believe have attractive prices and desirable correlation and volatility characteristics.

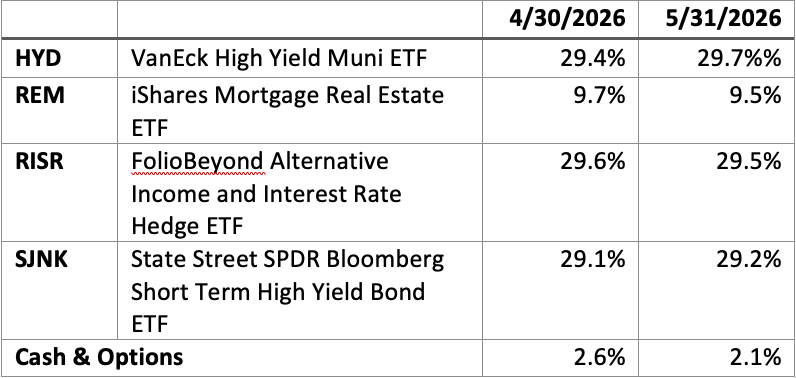

For the month of May, FIXP returned -0.22% (-0.08% based on NAV). On a YTD basis, FIXP is now outperforming the Bloomberg U.S. Bond Market Aggregate Index by 116 bps. There were no reallocations during the month, aside from those caused by differential performance.

FIXP’s performance was driven principally by adverse performance of REM, an ETF that holds mortgage REITS. REM has for some time exhibited greater volatility than FIXP’s other holdings, but it provides significant diversification as well as an attractive 9% dividend. The option overlay did not contribute meaningfully to overall performance during the month.

The fund’s holding weights are produced by FolioBeyond’s dynamic reallocation model. Changes are made from a universe of 24 economically diverse fixed income ETFs, based on volatility, momentum, yield, default risk, and other factors and occur based on market observations rather than a fixed schedule.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance and may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained by calling 866-497-4963. Short-term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. Returns beyond 1 year are annualized.

A fund's NAV is the sum of all its assets less any liabilities, divided by the number of shares outstanding. The market price is the most recent price at which the fund was traded. The fund intends to pay out income, if any, monthly. There is no guarantee that these distributions will be made.

Total Expense Ratio is 1.03%.

For FIXP standardized performance and fund holdings click here.

The allocation model that FIXP uses has been running for private clients and model portfolios for more than three years, and we are very excited to be bringing this advanced algorithm to ETF investors. Please reach out to us to learn more and to obtain detailed information and fund documents.

Market Review and Outlook

As the war between the US and Iran drags on, it has grown in importance as a market driver. This is due both to fundamental factors related prices for crude oil and derivative products such a fertilizers, as well as geo-political factors. Both factors haven driven by the news cycle and especially by social-media postings by President Trump and others. This is the first significant military conflict in which social media has played such an outsized role. It will likely not be the last.

Parties in both the US and Iran have attempted to influence the resolution of the conflict through social media postings that are a mix of truth, outright dishonesty and everything in between. Iran actors have shown themselves to be particularly adept at “trolling” the US and President Trump, specifically via animated posts mocking the inability of the US to achieve a decisive military control over the Strait of Hormuz. The legacy media has been forced to contend with social media as a source of information because it has been one of the primary ways the combatant parties have chosen to get their message out.

As a result of this new phenomenon, markets have reacted strongly—both positively and negatively—especially to posts on X and Truth Social, sometimes with astonishing speed. It has become commonplace to see equity, bond and commodity markets react almost immediately to social media postings. No doubt, part of this is due to algorithms that receive a continuous feed of social media traffic and then use AI to try to discern sentiment from the posts. In addition, while there has been no definitive proof, there has been speculation that both the US and Iran are aware of this new tactic and are using it in a manipulative fashion to move markets. Regulators in the US have opened investigations into a number of extremely well-timed trades that have generated enormous profits just prior to a market moving social media post. The suggestion is that insiders with knowledge of the upcoming posts are front-running. If true, this would be illegal in the US, but oil, Treasury bonds and equities trade around the world and around the clock, so there may be little US regulators can do to thwart this type of behavior in the short run.

For ordinary investors and for us, this is mostly noise. It does, however, add an element of volatility to markets that is unwelcome, to say the least. We have to remain attuned to the near constant flow of social media chatter, but we do mostly attempt to look through it, responding only when we identify a real signal. While it doesn’t affect our strategies, it can and has affected the timing of trades. For example, if bond yields overreact to some unsubstantiated bit of news that drives prices away from fundamentals, we may hold off on placing buy or sell orders until some clarity is reached. This is perfectly normal and routine behavior for any prudent and cautious investor. The difference now is that the frequency of such market moving “news” has increased greatly since the start of the war. It seems that this is the new reality for investor and is likely to persist even after the conflict ends.

Federal Reserve

As we noted above the Federal Reserve has a new Chair, Kevin Warsh who was sworn into office in May. Mr. Warsh previously served on the Fed’s Board of Governors, during the time of the Great Financial Crisis of 2008-09 (“GFC”). A lawyer by training (like Jerome Powell), Warsh worked in M&A at Morgan Stanley, and as an economic advisor during the second Bush Administration prior to his time at the Fed. Off the board since 2011, he has most recently been at the “conservative-lite” Hoover Institution at Stanford University. He is generally well-respected by markets and policy makers in D.C.

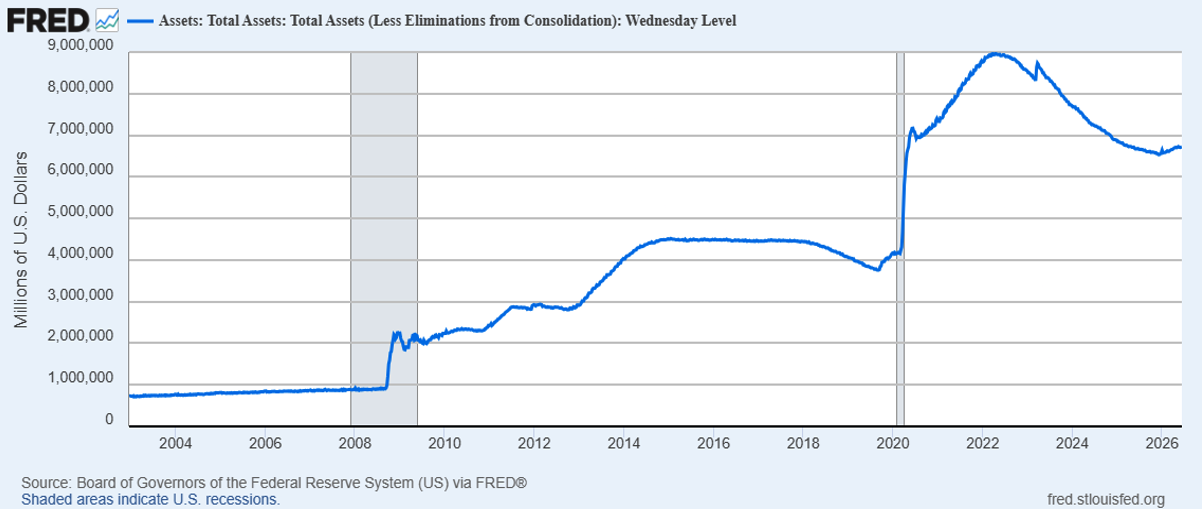

Warsh is difficult to slot specifically into a hawk/dove box, as he has expressed an eclectic mix of policy positions over the years. During the GFC he advocated for some Fed interventions to preserve systematically important institutions, but he argued against the massive interventions that drove interest rates to near zero, and kept them there for far too long. More recently he has argued that the Fed plays too large a role in the functioning of financial markets, and that a smaller, less active, and less visible Fed would be better for markets and the economy. He has been especially critical of the massive ballooning of the Fed’s balance sheet which still stands at more than $6.5 trillion, some 18 years after the GFC and 6 years after the covid pandemic.

The problem for Warsh and the Fed is that any attempt to meaningfully reduce the Fed’s balance sheet means selling bonds, which put downward pressure on prices, and upward pressure on interest rates. Meanwhile, inflationary pressure from the Iran war oil-shock is another force tending to push rates higher. The same pressures are coming from a gradually strengthening labor market.

President Trump and Treasury Secretary Bessent, of course, have made it abundantly clear they would like to see lower interest rates. Both have been extremely critical of former Chair Powell’s stewardship of a Fed that raised rates to fight post-covid inflation, and that has kept rates above the Administration’s preferred levels for more than a year. Given the economic environment, and the fact that he is one vote out of 19, Warsh would seem to have little ability to satisfy the president and the secretary, at least for the next several meetings. We will get our first official hearing from Warsh on June 18, following the upcoming FOMC meeting.

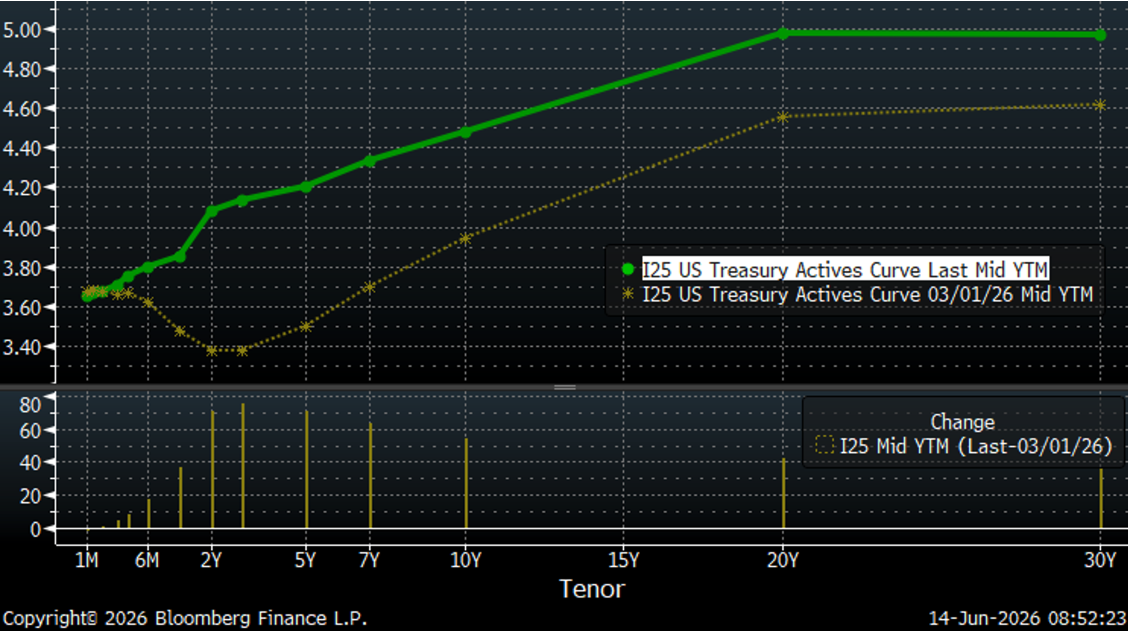

It is our belief the Fed’s hands are tied. Cutting short-term rates now, risks over-stimulating the economy, spurring further inflation expectations, and causing the economically important longer-term rate to rise further. Yields have increased at nearly all maturities since the start of the war, and even if the kinetic phase ends soon, the impacts of the supply shocks are likely to persist. We believe this makes it exceedingly unlikely that the Fed will be able to cut rates for the balance of 2026, and perhaps longer.

US Treasury Yields

One change that Chair Warsh could make, and has suggested he will implement, is to greatly reduce the amount of foreshadowing the Fed does about its intentions. Ever since Ben Bernanke was Chair, the Fed has adopted the view that frequent and fulsome communication from the Fed about forecasts, intentions, contingencies, etc., is useful to the market. There is an alternative view that too much communication, much of which is speculative and does not reflect true consensus at the Fed, actually is adding noise and volatility to the markets. It may also reduce the Fed’s ability easily to pivot or respond to unforeseen events. Warsh has publicly expressed support for this latter line of reasoning. Furthermore, he has stated that the Fed may be “too active” and that not every macro-economic event is a “crisis” requiring an affirmative response from the Fed.

It will be interesting to see how the market will adapt to this approach, if he actually does take it, since it differs significantly from that taken by the Fed going back at least 20 years.

Meanwhile, inflationary pressures continue to mount. Only due in part to the direct war impacts, there is strong evidence of strain on household budgets. Several major retailers and fast-food operators have noted that consumers are aggressively economizing on a wide range of purchases. Credit card delinquencies continue to rise. Meanwhile Federal deficit spending is accelerating, with the Trump Administration is suggesting another $350-500 billion military supplement may be needed. There is no longer any political constituency in Washington for fiscal restraint. Both parties have staggering spending goals. The only differences are with respect to their budgetary priorities.

This trend is deeply embedded into the fabric of American politics, and ending the campaign in Iran, will have no material effect. Indeed, the idea of a $300 billion Iran “recovery” spending program has been floated. While that may be a bridge too far for American taxpayers, it goes to show the extent to which any notion of budgetary discipline has evaporated. The deficit will have to be funded, and that means the Treasury will have to sell an unprecedented volume of government bonds to the rest of the world. And this comes at a time when the rest of the world is seriously questioning the credit-worthiness of the US, and is actively looking for ways to diversify. But in the aggregate, there can be no net reduction in the amount of US debt held by the rest of the world, as long as the US continues to run trade deficits. It can only be reallocated and shifted among creditors. And as new debt comes to market, the only way to attract buyers is through higher yields. It is simple supply and demand at work.

There has been some futuristic theorizing, including from Kevin Warsh, that AI will usher in an era of abundance and productivity so profound that, in the longer-term, the US may actually have to contend with widespread deflation. AI has shown its utility in a number of contexts, and various parties have expressed ambitions for investing hundreds of billions or even trillions of dollars in data centers. But in terms of national productivity statistics, and even corporate financial reports, there is little if any evidence of this so far.

One is entitled to be a bit skeptical of outlandish projections from businesses seeking to raise hundreds of billions in IPOs and private capital. Like many prior technical revolutions, from the railroads to electrification, the true benefits will take decades to manifest. In the meantime, eventual productivity-induced deflation is not something investors with finite time horizons need to concern themselves with.

Summary

Risks abound in the current environment. The outlook as of now, is for major change in Washington from the upcoming mid-term elections. If the Democrats take both chambers as betting odds now favor, we can expect a level of political battle that will make Trump’s first half look like a pillow fight. One can’t rule out an impeachment bill being among the first actions of a newly-Democratic House. The conflict between the US and Iran, currently teetering on a fragile cease-fire, is going to be with us for at least the balance of 2026, and probably much longer. Meanwhile the government spends with abandon, and there is little if anything the Fed can do to counter the adverse effects from that.

There is a well-established playbook for this type of environment. Protect your capital and look for investments that generate current cash income. Trying to trade the news or time the markets in such an environment is reckless in the extreme. The news will always be faster and more unpredictable that you are as an investor.

Please contact us to explore how RISR and FIXP might fit into your overall strategy, to help you manage risk while generating an attractive current yield.

Performance

Portfolio Applications

We believe RISR and FIXP can provide attractive, thematic strategies that provide strong correlation benefits for both fixed income and equity portfolios. They can be utilized as part of a core holdings for diversified portfolios or as an overlay to manage the risks of fixed income portfolios. RISR can be used as a macro hedge against rising interest rates with less exposure to equity beta and negative correlation to fixed income beta. The underlying bonds are all U.S. agency credit that are guaranteed by FNMA, FHLMC or GNMA. Also, timing is on our side as the strategy generates current income if interest rates were to remain within a trading range. FIXP offers a broadly diversified exposure to multiple sectors of the fixed income markets in an algorithmically optimized manner.

Please contact us to explore how RISR and FIXP can be utilized as a unique tool to adjust your portfolio allocations in the current high volatility environment.

| Yung Lim | Dean Smith | George Lucaci |

|---|---|---|

| Chief Executive Officer | Chief Strategist and Marketing Officer | Global Head of Distribution |

| Chief Investment Officer | RISR Portfolio Manager | |

| ylim@foliobeyond.com | dsmith@foliobeyond.com | glucaci@foliobeyond.com |

| 917-892-9075 | 914-523-2180 | 908-723-3372 |

This material must be preceded or accompanied by a prospectus. For a copy of the prospectus please click here for RISR and here for FIXP.

Investments involve risk. Principal loss is possible. Unlike mutual funds, ETFs trade at a premium or discount to their net asset value. The fund is new and has limited operating history to judge fund risks. The value of MBS IOs is more volatile than other types of mortgage related securities. They are very sensitive not only to declining interest rates, but also to the rate of prepayments. MBS IOs involve the risk that borrowers default on their mortgage obligations or the guarantees underlying the mortgage-backed securities will default or otherwise fail and that, during periods of falling interest rates, mortgage-backed securities will be called or prepaid, which result in the Fund having to reinvest proceeds in other investments at a lower interest rate.

The Fund’s derivative investments have risks, including the imperfect correlation between the value of such instruments and the underlying assets or index; the loss of principal, including the potential loss of amounts greater than the initial amount invested in the derivative instrument. The value of the Fund’s investments in fixed income securities (not including MBS IOs) will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed income securities owned indirectly by the Fund. Please see the prospectus for a complete description of principal risks.

FIXP Risks

Underlying ETFs Risks. The Fund will incur higher and duplicative expenses because it invests in underlying ETFs, including Bond Sector ETFs and broad-based bond ETFs (collectively, “Underlying ETFs”). There is also the risk that the Fund may suffer losses due to the investment practices of the Underlying ETFs. The Fund will be subject to substantially the same risks as those associated with the direct ownership of securities held by the Underlying ETFs.

Fixed Income Risk. The prices of fixed income securities respond to economic developments, particularly interest rate changes, as well as to changes in an issuer's credit rating or market perceptions about the creditworthiness of an issuer. In general, the market price of fixed income securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter-term securities.

Option Overlay Risk. The Fund's use of options involves various risks, including the risk that the options strategy may not provide the desired increase in income or may result in losses. Selling call and put options exposes the Fund to potentially significant losses if market movements are unfavorable. The Fund may also experience additional volatility and risk due to changes in implied volatility (the market's forecast of future volatility), strike prices, and market conditions. The Fund may sell options on instruments other than the Fund's Bond Sector ETFs. This can expose the Fund to the risk that options can vary in price in ways that do not correspond to the Bond Sector ETFs held by the Fund, so called basis-risk.

Interest Rate Risk. Generally, the value of fixed income securities will change inversely with changes in interest rates. As interest rates rise, the market value of fixed income securities tends to decrease. Conversely, as interest rates fall, the market value of fixed income securities tends to increase.

New Fund Risk. The Fund is a recently organized management investment company with no operating history. As a result, prospective investors do not have a track record or history on which to base their investment decisions.

Diversification does not eliminate the risk of experiencing investment losses.

Index Definitions

Bloomberg Barclays US Aggregate Bond Index: A broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

US Treasury 7-10 Yr Bond Inversed Index: ICE U.S. Treasury 7-10 Year Bond 1X Inverse Index is designed to provide the inverse of the daily return of the ICE U.S. Treasury 7-10 Year Bond Index (IDCOT7). ICE U.S. Treasury 7-10 Year Bond Index tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market. Qualifying securities of the underlying index must have greater than or equal to seven years and less than 10 years remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and an adjusted amount outstanding of at least $300 million.

S&P 500 Index: The S&P 500 Index, or Standard & Poor's 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

IBOXHY Index: iBoxx USD Liquid High Yield Total Return Index measures the USD denominated, sub-investment grade, corporate bond market. The index includes bonds with minimum 1 years to maturity,

minimum amount outstanding of USD 400 mil. Bond type includes fixed-coupon, step-up, bonds with

sinking funds, medium term notes, callable and putable bonds.

Definitions

Alpha: a return achieved above and beyond the return of a benchmark or proxy with a similar risk level.

Annualized Equivalent Yield: represents the annualized yield based on the most recent month of income distribution: (income distribution x 12 months)/price per share.

Basis Points (bps): Is a unit of measure used in quoting yields, changes in yields or differences between yields. One basis point is equal to 0.01%, or one one-hundredth of a percent of yield and 100 basis points equals 1%.

Beta measures: the volatility of a security or portfolio relative to an index. Less than one means lower volatility than the index; more than one means greater volatility.

Convexity: A measure of how the duration of a bond changes in correlation to an interest rate change. The greater the convexity of a bond the greater the exposure of interest rate risk to the portfolio.

Correlation: a statistic that measures the degree to which two securities move in relation to each other.

Coupon: is the annual interest rate paid on a bond, expressed as a percentage of the bond’s face value.

CUSIP: An identifier number that stands for the Committee on Uniform Securities Identification Procedures assigned to stocks and registered bonds in the United States and Canada.

Duration: measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

GNMA: Government National Mortgage Association

FNMA: Federal National Mortgage Association

FHLMC: Federal Home Loan Mortgage Corporation

Short Investment (Shorting): is a position that has been sold with the expectation that it will decrease in value, the intention being to repurchase it later at a lower price.

Distributed by Foreside Fund Services, LLC.